Challenges to Chokepoints

Does controlling ASML really get you leverage?

Welcome to Features and Targets! This is my first post. I’m a Kennedy Scholar at Harvard, focusing on AI and geopolitics. I previously led policy work at the UK AI Security Institute (AISI).

This piece is a preview of a forthcoming paper that asks whether controlling supply chain ‘chokepoints’ really gets you leverage, based on interviews with senior former US and Dutch Government officials.

I’ll be sharing pieces like this roughly monthly, covering AI progress and its impacts on the balance of power. Do subscribe if that sounds useful!

This post reflects my personal views. Feedback is strongly encouraged, in the comments or directly. Let’s get started!

- Dylan

An ASML EUV lithography machine. Credit: ASML.

TL;DR

AI progress and increased risk of weaponized interdependence is causing middle powers to seek ‘sovereign AI’. Controlling supply chain ‘chokepoints’ is emerging as a dominant strategy to achieve sovereign AI.

The extent to which middle powers can actually leverage control of chokepoints has not been empirically tested. This post uses the case study of US-Dutch export control negotiations to test whether ‘most likely’ chokepoint ASML really yields leverage.

Evidence from interviews with senior former US and Dutch Government officials demonstrates that ASML yields little leverage in isolation. But this case study does point to a broader set of conditions middle powers must meet to exercise influence today.

Introduction

‘I can’t comment on the nature of the talks. But the US can’t simply impose such changes on us. We participate in these talks in a sovereign manner. Because the Americans need us too.’

Dutch Minister for Foreign Trade, Liesje Schreinemacher, November 2022

AI progress is accelerating at a moment of rupture in international relations. The global economy is transitioning from a neoliberal order to a new geoeconomic order, characterized by greater focus on relative over absolute gains. A key attribute of the geoeconomic order is a greater tendency for states to both weaponize interdependence and seek to reduce exposure to weaponization.

The combination of accelerating AI capabilities and increased risk of weaponized interdependence is causing middle powers to seek ‘sovereign AI’. Sovereign AI starts from the assumption that middle powers cannot rely on the US or China for access to advanced AI. Yet there remains no settled definition. I’ll define sovereign AI as the capability to ensure advanced AI development and deployment adheres to the norms, laws and values of the state and creates domestic economic value.

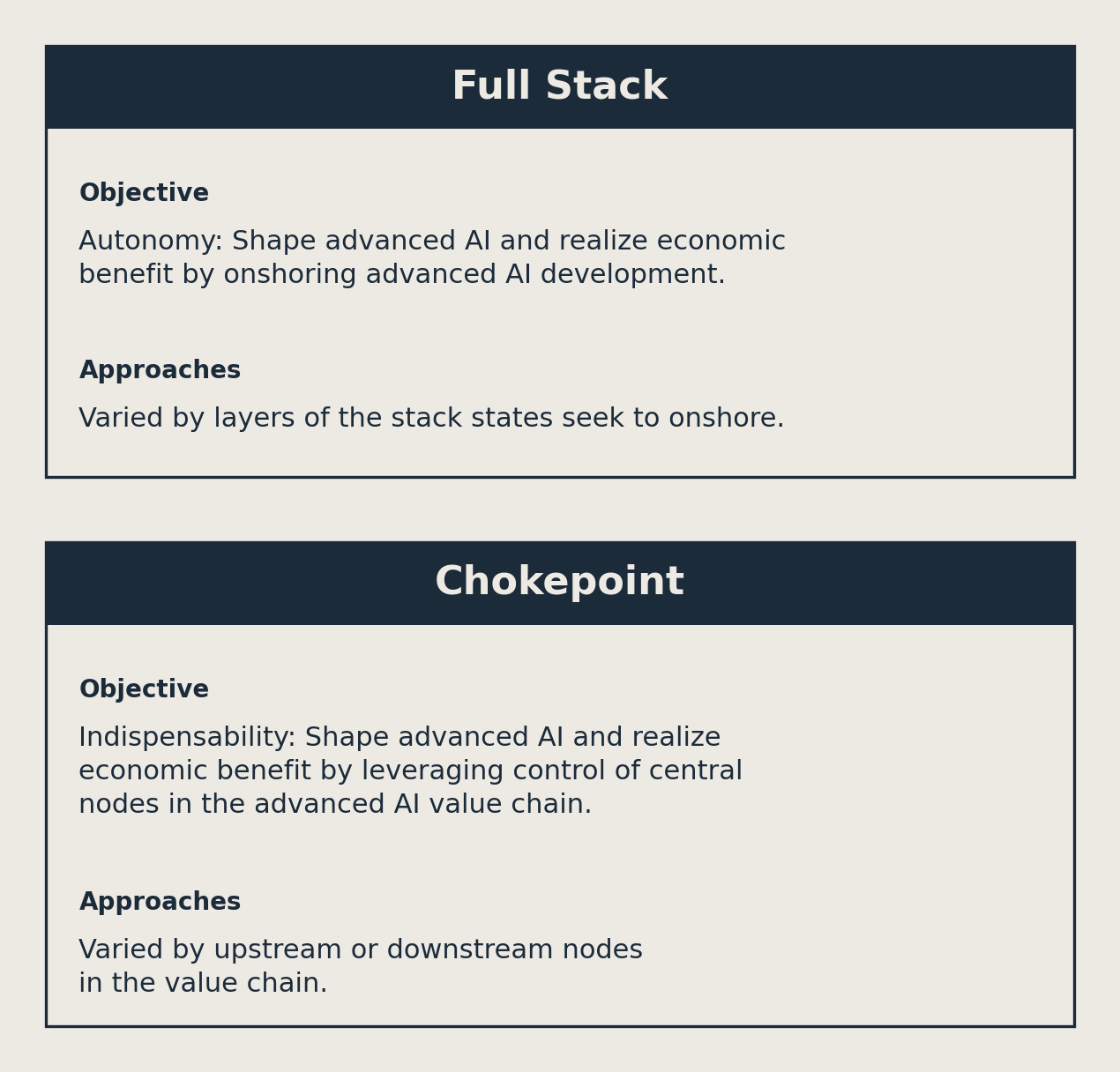

Two broad approaches are emerging for middle powers to achieve ‘sovereign AI’. ‘Full stack’ strategies seek autonomy from the US and China. They aim to shape advanced AI and realize economic benefit by onshoring AI development. The challenges of full stack strategies are well documented. Onshoring compute exchanges dependence for access to advanced AI with dependence for access to hardware and maintenance. Domestically developed AI systems will lag the US and Chinese leaders.

‘Chokepoint’ strategies have been proposed as an alternative. Where full-stack strategies seek autonomy, chokepoint strategies seek indispensability. They aim to shape advanced AI and realize economic benefit by leveraging control over central nodes in the AI value chain. Middle powers may focus on controlling nodes upstream (in the semiconductor supply chain) or downstream (in complementary assets, such as autonomous labs) of advanced AI systems. Leverage is operationalized as the ability to alter or constrain decision-making by leading powers, and stems from the latent risk that the middle power will weaponize interdependence.

Chokepoint strategies sound sensible. Rather than competing with the US or China to develop advanced AI systems, seize a stake in the value chain. Yet the extent to which middle powers can actually leverage control of chokepoints has not been empirically tested. This matters as states mobilize billions to achieve sovereign AI.

From 2022-2024, the US and the Netherlands negotiated export controls to prevent the sale of ASML DUV immersion lithography machines to China. ASML is widely recognized as a chokepoint in the semiconductor supply chain (former Prime Minister Rishi Sunak has even suggested an ‘ASML strategy’ of ‘occupying choke points’). This case study allows us to test the extent to which middle powers can actually leverage control of chokepoints. Did ASML give the Netherlands negotiating leverage? If even ASML does not confer meaningful leverage, where does that leave middle powers?

I spent a few weeks researching and speaking to senior former US and Dutch Government officials involved in the negotiations to find out.

ASML is a ‘Most Likely’ Chokepoint

ASML is a semiconductor manufacturing equipment (SME) company based in the Veldhoven, the Netherlands. ASML specializes in lithography machines that ‘print’ circuit patterns onto silicon wafers.

Lithography works by projecting light onto a wafer using a mask. When light passes through (or reflects off) the mask, the pattern on the mask is projected onto a wafer. The wafer is covered with photoresist that reacts with the light (hardening or softening). The wafer is then washed to remove softened photoresist, and exposed to a corrosive chemical to etch a circuit pattern. The remaining hardened photoresist is then removed, and the process is repeated.

More advanced semiconductors require lithography machines to project patterns with smaller features. This requires shorter wavelengths of light. ASML produces two main types of lithography machine: DUV immersion machines, which project light at a wavelength of 193 nanometres (nm) and can be used to produce chips at process nodes between 40nm and 7nm; and extreme ultraviolet (EUV) machines, which project light at a wavelength of 13.5nm and can be used to produce chips at process nodes at or below 5nm.

ASML is widely recognized as a chokepoint in the semiconductor supply chain. I’ll define a chokepoint as a central node in the AI value chain with low elasticity of demand. This creates a simple set of criteria: a chokepoint asset should have limited substitutes, high barriers to entry, and be difficult to innovate around. ASML clearly meets these criteria.

Limited Substitutes

ASML has a total monopoly over EUV machines and a dominant market share in DUV immersion machines, competing only with Nikon. ASML produces 100% of the global supply of EUV machines.

ASML’s monopoly is a product of persistent engineering, acquisition strategy, and historical accident. In 1996, Congress cut Department of Energy funding for EUV research. Intel stepped in to fill the gap, creating the EUV-LLC consortium. ASML began investing in EUV around the same time. In 1998, ASML and Zeiss created the Euclides consortium for EUV. The EUV-LLC and Euclides consortia merged in 1999. Intel supported the merger as it would broaden the supplier base for future EUV machines. The leading US lithography company, Silicon Valley Group, was already part of the EUV-LLC consortium. Tensions with Japan precluded Nikon and Canon joining. ASML was therefore a welcome addition, and was awarded a license to manufacture EUV machines. Two years later, ASML completed the acquisition of Silicon Valley Group, complete with its EUV license. ASML was now the only lithography company with access to US patents.1

Barriers to Entry

Cost, complexity and culture make ASML difficult to replicate. R&D spend to develop EUV has been estimated in the tens of billions of dollars. To sustain R&D spend, ASML has been supported by the Dutch Government and other companies in the semiconductor supply chain. The Ministry of Economic Affairs facilitated the creation of ASML in 1984 as a joint venture between electronics firm Philipps and trading house ASM International. In the early years, around half of ASML’s research budget came from government subsidies.2

Complexity explains much of the cost of developing lithography machines. To create a stable source of EUV light, a droplet of tin must be heated to 220,000 degrees Celsius, using a laser that strikes each droplet twice at a frequency of 50,000 times per second. Each EUV light source contains over 450,000 individual components, and can only be built by US-based Cymer with German laser-maker Trumpf. EUV light is absorbed by air and glass, so must be reflected through a vacuum using mirrors composed of hundreds of layers, each nanometres thick. Zeiss has a monopoly on the mirrors used in EUV machines.

A visualisation of an EUV lithography machine. Credit: ASML.

Culture also makes ASML hard to reproduce. Engineers are deployed alongside ASML machines, making access to tacit knowledge as much a product as the machine itself. Skills such as replacing the wiring around the ‘nozzle’ of the EUV light source cannot be automated and must be learned from experience.3 This tradition of knowledge can be traced back to the ‘Nat Lab’ at Philipps.

Difficult to Innovate Around

Various alternatives to ASML EUV machines have been proposed, including multi-e-beam (MEB), nanoimprint (NIL) and directed self-assembly (DSA) approaches. Yet these approaches face challenges.

NIL is the most frequently cited. Where EUV uses light to print circuit designs, NIL physically ‘stamps’ designs onto silicon wafers. Yet this requires ‘stamps’ that do not degrade despite the miniscule features they inscribe on the wafer. This remains an unsolved problem despite persistent investment by Canon. Analysts have therefore concluded that NIL will not soon replace EUV for leading-edge production.

ASML is a ‘best case’ chokepoint for a middle power. It is such a strong chokepoint it must surely give the Dutch the ability to constrain or alter decision-making by the US or China. Negotiations between the US and the Netherlands regarding exports of DUV immersion machines to China let us test this theory.

The Case of US-Dutch Negotiations

I’ll start with a brief summary of export control negotiations between the US and the Netherlands, before making the positive and negative case for Dutch leverage.

In October 2022, the US imposed controls on 11 types of US-origin SME relevant to producing ‘advanced node semiconductors’. The US then encouraged allies to adopt equivalent controls. President Biden raised DUV immersion controls with Prime Minister Rutte during a White House meeting in January 2023. Later that month, National Security Advisor Jake Sullivan concluded an unpublished deal with the Dutch to limit exports of DUV immersion machines to China.

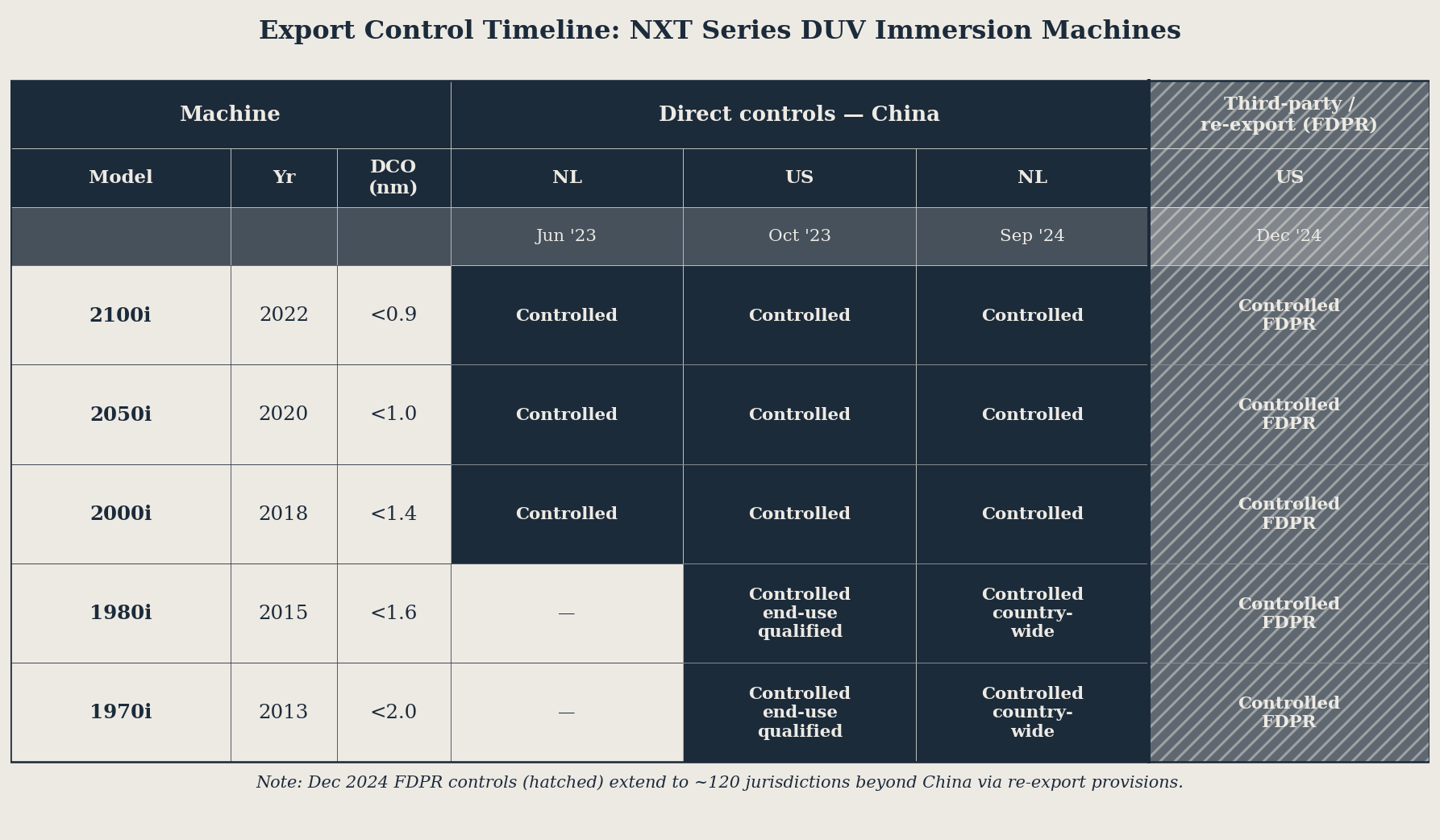

The Dutch imposed export controls in June 2023. Licenses were required for the export of lithography machines with ‘wavelength of the light source equal to or longer than 193nm’ and a maximum dedicated chuck overlay (DCO) value ‘less than or equal to 1.50nm’. DCO is a measure of how precisely a machine aligns a new circuit pattern over a previous one (lower is better). This captured the most advanced ASML DUV immersion machines, the NXT:2100i, NXT:2050i and NXT2000i.

In October 2023, the US issued an update to its October 2022 controls. This created a 0% de minimis rule requiring licenses for the export of lithography machines with ‘a light source wavelength equal to or longer than 193nm’ and a maximum DCO value ‘greater than 1.50nm but less than or equal to 2.4nm’ if destined for use in advanced node production. This captured less advanced ASML DUV immersion machines, including the NXT:1980i and NXT1970i, asserting US extraterritorial jurisdiction over Dutch-produced technology.

The Dutch responded in September 2024. New export controls required licenses for the export of lithography machines with ‘wavelength of the light source equal to or longer than 193nm’ and a maximum DCO value ‘greater than 1.50nm and less than or equal to 2.4nm’. This aligned US and Dutch controls, disapplying US extraterritorial jurisdiction.

The US issued a final round of controls in December 2024, using the foreign direct product rule (FDPR). The FDPR allows Commerce to impose export controls on foreign-produced goods manufactured with US technology or software. The ‘SME’ and ‘FN5’ FDPRs controlled the re-export of ASML machines from third countries.

A timeline of export controls on DUV immersion lithography machines.

Leverage Realized?

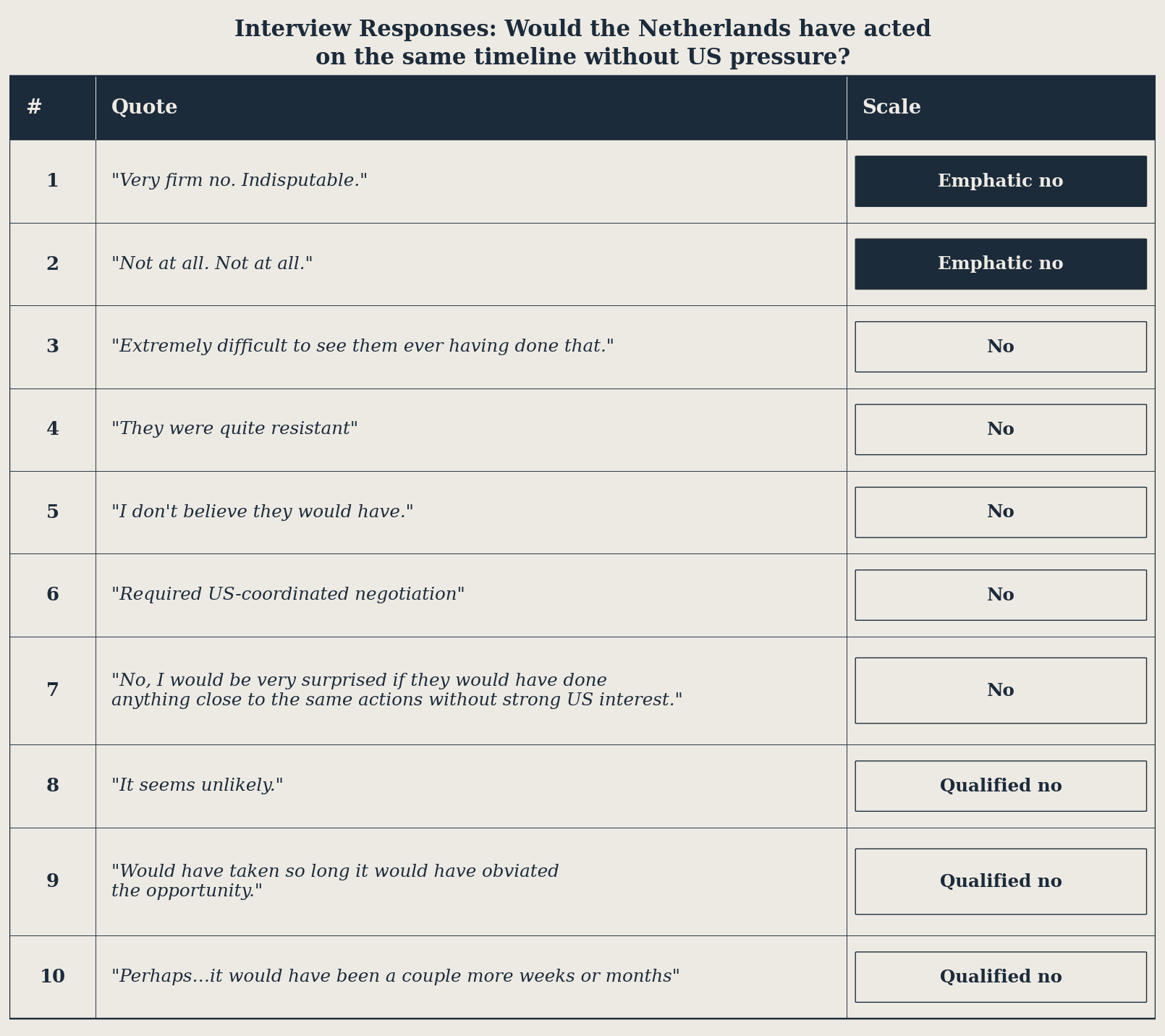

The Dutch Government would not have imposed export controls on DUV immersion machines on the same timeline absent US pressure. While the Dutch position on China did harden over time, Dutch strategy emphasized reducing import dependencies rather than controlling exports. Imposing export controls also came with costs: ASML spent 16bn euros on suppliers in 2024, mostly within the Netherlands and the EU. The same year, 70% of DUV immersion machine sales came from China.

Interviews for this post supported the conclusion that the Dutch would not have acted without US pressure. As one former US official put it, ‘the Netherlands was doing this because the United States was forcing them to’.

Coded responses to the question of whether the Netherlands would have imposed export controls on DUV immersion lithography machines on the same timeline absent US pressure.

Lack of alignment leaves the Dutch negotiating with the US. On the surface, it seems as if the Dutch Government was able to leverage ASML to constrain or alter US decision-making. The latent risk of Dutch weaponization changed outcomes.

The October 2022 export controls imposed by the US can be viewed as concession to get Dutch support. The controls placed US firms at a competitive disadvantage, with Lam Research the worst effected. They also addressed a longstanding Dutch concern, that US deposition and etching equipment was allowing Chinese firms to compensate for lack of access to EUV machines (which had been export controlled since 2019).

US officials publicly described the controls as a concession to secure Dutch support. In October 2022, Under Secretary for Commerce Alan Estevez said ‘what we keep hearing is to ensure that you also, US, have skin in the game. We’ve shown we have skin in the game, we’ve taken action, we’ve viewed it as a down payment for what we’re going to do’. Former officials made similar arguments in interviews for this post. One described the controls as a ‘bet’ to get the Dutch ‘to agreement relatively rapidly’. Another commented that the controls showed ‘we are willing to take the hit ourselves to show you this is important’.

The implementation of the deal agreed in January 2023 also seems to suggest Dutch leverage. Significant time elapsed between the deal being agreed and Dutch export controls on DUV immersion machines being imposed in June 2023. Even after export controls were imposed, ASML was permitted to continue shipping DUV immersion machines to China. The Dutch Government issued new licenses in September 2023 that allowed ASML to make shipments through January 2024. ASML sales to China spiked over this period. Reports suggest that 21 DUV machines were shipped to China in October 2023 and 16 in November 2023. In FY2023, China represented 29% of ASML sales, doubling from 14% in 2022. China represented 45% of DUV immersion machine sales in 2023, up from 26% in 2022.

The imposition of the 0% de minimis rule in October 2023 seems to show the limits of Dutch leverage. The rule asserted US extraterritorial jurisdiction over Dutch technology to prevent exports to China. Yet even this rule can be understood as a demonstration of Dutch leverage. First, there was a long period between the initial deal between the US and the Netherlands and the imposition of 0% de minimis. Second, the rule shielded the Dutch Government from Chinese retaliation. It allowed the Dutch to claim they were being coerced by the US.

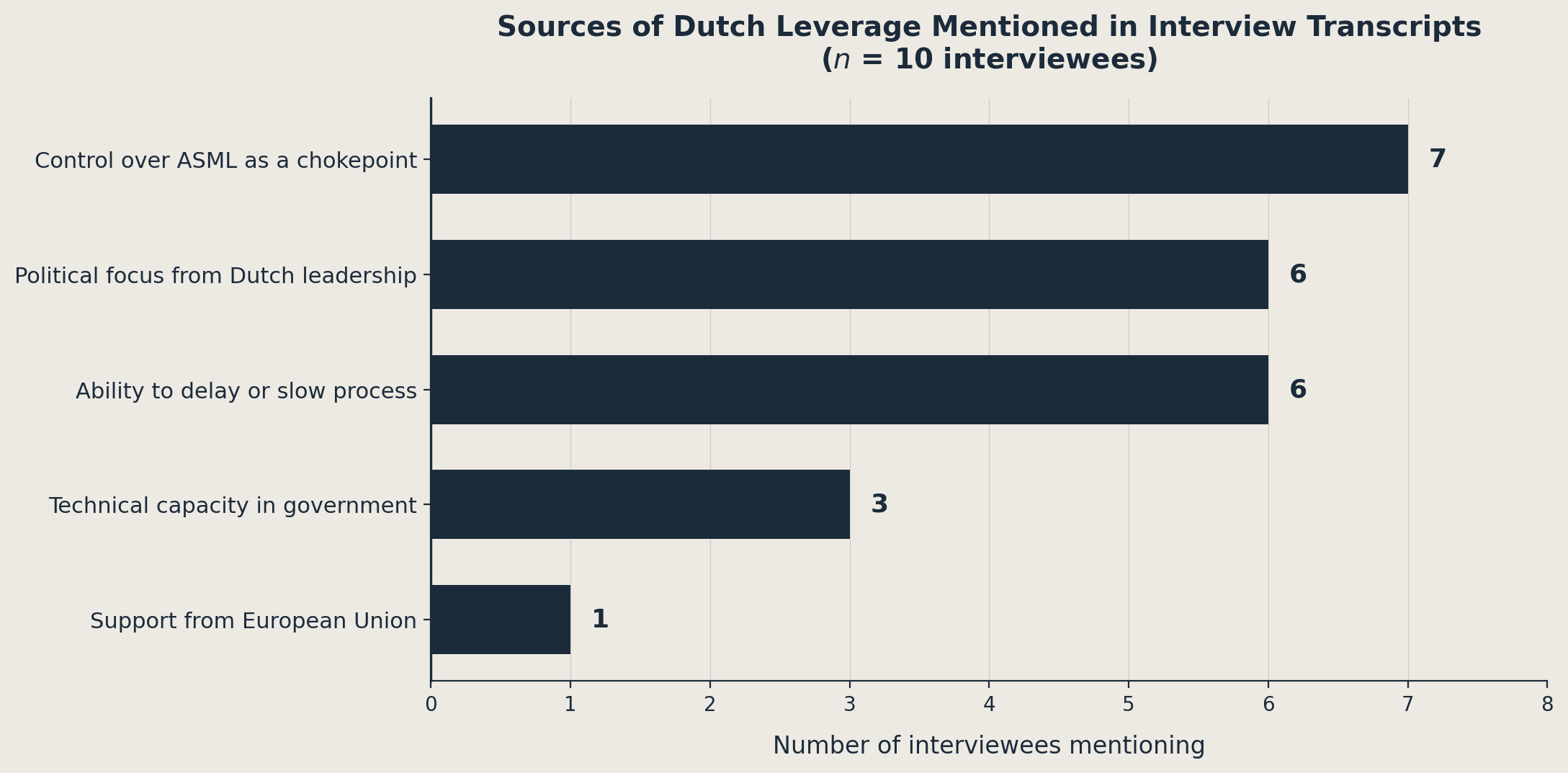

Taken together, these factors seem to suggest that the Dutch Government had meaningful leverage in negotiations with the US. Interviewees cited several sources of Dutch leverage. The importance of Dutch control over ASML was recognized by both US and Dutch officials. Yet other factors also played a role, including strong technical capacity (‘small but smart set of officials…able to go toe to toe on a lot of questions’); close relations between the Dutch Government and ASML (joining calls together, negotiating with the US jointly); and personal focus from Prime Minister Rutte and Dutch National Security Advisor Geoffrey van Leeuwen.

Sources of Dutch leverage identified by US and Dutch interviewees for this post.

Leverage Denied

Yet a closer analysis illustrates the limits of Dutch leverage. The October 2022 controls would not have been implemented unless the US believed they would have a meaningful impact on Chinese chip production. The implementation timeline for the January 2023 deal was fully agreed in advance. What looks like leverage was actually a coordinated, multi-step process. And licenses allowing ASML to scale shipments to China were revoked soon after the US became aware of them. As one former US official explained diplomatically, ‘there was a conversation about what was committed to and that somehow that commitment was garbled or misunderstood or not totally embraced’. Commerce Secretary Gina Raimondo was less diplomatic in a meeting with ASML CEO Peter Wennink in November 2023.

Nor was there perfect alignment between the Dutch Government and ASML. According to one US official, Wennink responded to US criticism by ‘throwing the Dutch Government under the table’. The Dutch Government was meanwhile surprised by the extent of DUV immersion machine sales to China. It has since been reported that Prime Minister Rutte spoke to Wennink in November 2023 to reprimand him personally (Wennink reportedly offered to spy on China). Licenses for the export of NXT:2050i and NXT:2100 machines were revoked in January 2024.

Partly due to the scale of ASML shipments to China in 2023, many former US officials reflected that they should have gone further, faster. One commented that ‘I think we probably should have gone all out earlier on’. Another noted that ‘if anything we should have gone faster’. Asserting extraterritorial jurisdiction through the FDPR was an option from the outset. As one official said, ‘it was very easy for us to implement the FDPR, we just chose not to’. According to another US official, the FDPR was a ‘pistol on the table’.

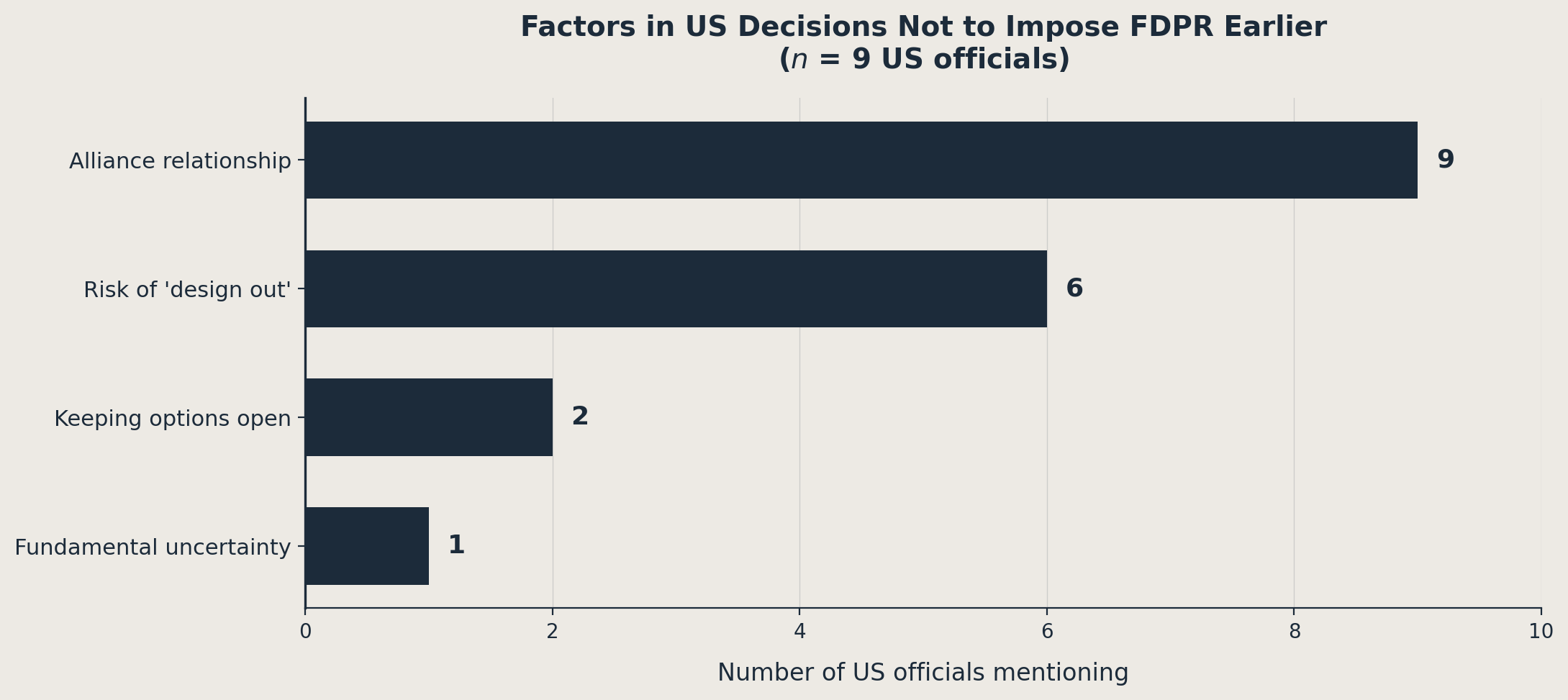

This raises the question of why the US did not impose the FDPR sooner. Officials gave several reasons. There was some concern that the FDPR would lead allies to ‘design out’ US components, reducing long-term US leverage.

Yet the dominant reason was the importance of the alliance network. The Biden Administration came to office promising to rebuild alliances. In his inaugural, Biden promised to ‘repair our alliances and engage with the world once again’. This approach, viewing allies as force multipliers, underpinned US foreign policy.

Former US officials have publicly stressed the importance of the alliance network to the FDPR decision. Former National Security Advisor Jake Sullivan has said that ‘we had a thesis with respect to our allies – you work with them rather than coerce them’. Former US officials also stressed the importance of alliances in interviews for this post. One commented that ‘Biden’s kind of natural instinct is just to be much more collegial and friendly to allies. But in hindsight, we probably could have pushed harder’. Another reflected that ‘I think it was an ideological commitment to alliances, recognizing the hard-to-measure benefits to the alliance of maintaining voluntary cooperation’.

Reasons not to impose FDPR mentioned in interview transcripts at least once.

Not a single former US official cited retaliation risk as a reason to delay the FDPR. Despite broad recognition that the Dutch Government controlled a chokepoint in the semiconductor supply chain, the threat the Dutch would weaponize dependence against the US did not feature in US decision making. ASML was seen as a source of leverage in the abstract, but the latent risk of Dutch weaponization did not actually alter or constrain US choices in practice.

Outlook

The absence of Dutch leverage is best understood through the lens of structural power. Susan Strange defines structural power as ‘the power to decide how things shall be done, the power to shape frameworks within which states relate to each other, relate to people, or relate to corporate enterprises’.4 Power over the ‘production structure’ entails the ability to decide ‘what shall be produced, by whom, by what means and with what combination of land, labour, capital and technology and how each shall be rewarded’.5 Strange contends that ‘information-rich occupations’ tend to confer greater power over the production structure, since they determine what can be manufactured further down the value chain.6

US dominance of chip design, plus continued influence across other segments, grants it structural power over the semiconductor supply chain. These two factors ensure there is always a nexus to US content, and give the US escalation dominance.

The nexus between ASML and the US is strong. ASML manufactures EUV machines under a license granted by the Department of Energy.7 ASML’s largest R&D base outside Europe is the former Silicon Valley Group campus at Wilton, Connecticut. The light source for EUV machines is produced by ASML subsidiary, Cymer, in San Diego, California. The e-beam metrology tools that allow wafer defects to be detected at EUV scale are developed by ASML-owned HMI in San Jose, California. Underpinning all of this are chips designed by US companies using US-origin Electronic Design Automation (EDA) software. ASML is dependent all the way down.

This nexus is what makes the FDPR so powerful, and undermines the ability of the Dutch Government to credibly threaten to weaponize ASML. Throttling or stopping deliveries of EUV machines would entail mutually assured destruction at best. The Dutch Government could cause the US significant pain, but only at the cost of ASML’s business. This is also before horizontal escalation by the US into other networks of dependence, such as finance or security.

Several interviewees noted this dynamic. One commented that the weaponization of ASML would ‘require a Dutch level of risk acceptance that they have not been prepared to show’. Another reflected that ‘the idea of the Dutch retaliating against us…exploiting interdependencies…was sort of hard to imagine. In the cycle of tit for tat, it’s hard to see the Dutch winning out’.

This should be a reality check for states seeking sovereign AI. US structural power means that even control over a chokepoint as critical as ASML may be insufficient for actual leverage.

To exercise meaningful leverage, a middle power must satisfy three conditions:

The middle power must control a chokepoint asset that leading powers cannot easily substitute.

The cost to the leading power of losing access to the chokepoint asset must be greater than the cost to the middle power.

The middle power must be able to withstand vertical or horizontal escalation by the leading power, at least for a relevant period of time.

These are hard conditions to meet.

This is not to say that chokepoints have no value for middle powers. ASML generates significant domestic economic benefit for the Netherlands. The company currently produces around 70 EUV machines p/a. As demand for compute grows, ASML is likely to become a key bottleneck to AI progress. Revenues will likely increase, and the company has space to charge much higher margins.

But domestic economic benefit is only half of the definition of sovereign AI I gave above. If chokepoints are insufficient alone, what else can middle powers do? What policies or investments will allow them to meet the ‘conditions for leverage’ ?

That will be a subject of a future post. Stay tuned!

Additional detail in Marc Hijink, Focus, 2023, pp.124-127; Chris Miller, Chip War, 2022, pp.183-191.

Marc Hijink, Focus, 2023, p.141.

Marc Hijink, Focus, 2023, p.141.

Susan Strange, States and Markets, 1988, p.25.

Susan Strange, States and Markets, 1988, p.29.

Susan Strange, The Future of the American Empire, 1988, p.5.

Marc Hijink, Focus, 2023, pp.126-127.

Really brilliant read

Learned a lot reading this